About us:

The CCAIA is the focal agency for the administration, operation, and implementation of Internal Audit services in government agencies. Following the transformation of the Civil Service, the services of Internal Audit are consolidated under the Ministry of Finance to strengthen and improve the Internal Audit services and address the high attrition rate. The consolidation of IA services was approved by the Royal Civil Service Commission (RCSC) on 25th April 2023.

The National Internal Audit Committee comprises of the following members:

1. Hon’ble Cabinet Secretary – Chairperson;

2. Secretary, Ministry of Finance – Member;

3. Director, RCSC – Member; and

4. Chief Internal Auditor, CCAIA – Member Secretary.

Definition of Internal Auditing

The Institute of Internal Audit (IIA), USA has defined Internal Audit as:

“Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes.”

Based on the IIA definition, the RGoB has accordingly defined the purpose of the Internal Audit in the Internal Audit Charter as:

“The Internal Audit Services conduct audits and reviews, using a systematic and disciplined

approach, to provide:

(i) Independent and objective assurance on the efficiency and effectiveness of their respective

Entity’s governance, risk management, control, and accountability processes.

(ii) Recommendations for improving the efficiency and effectiveness of the

Entity’s operations, achieving organizational objectives, and proper stewardship of

resources.

Mission :

The mission of the Internal Audit Service is to provide the management in Government organizations with independent, objective assurance and consulting services designed to add value and improve an organization’s operation.

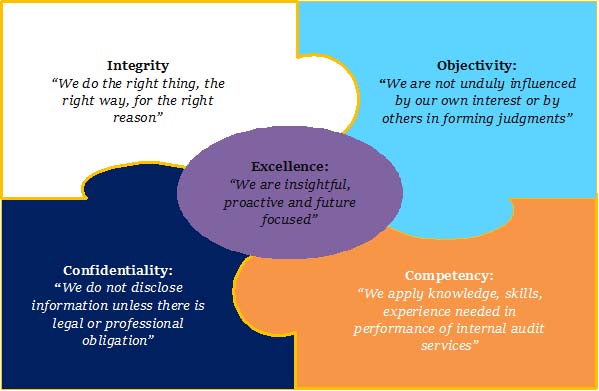

Core Values:

{kind=link}

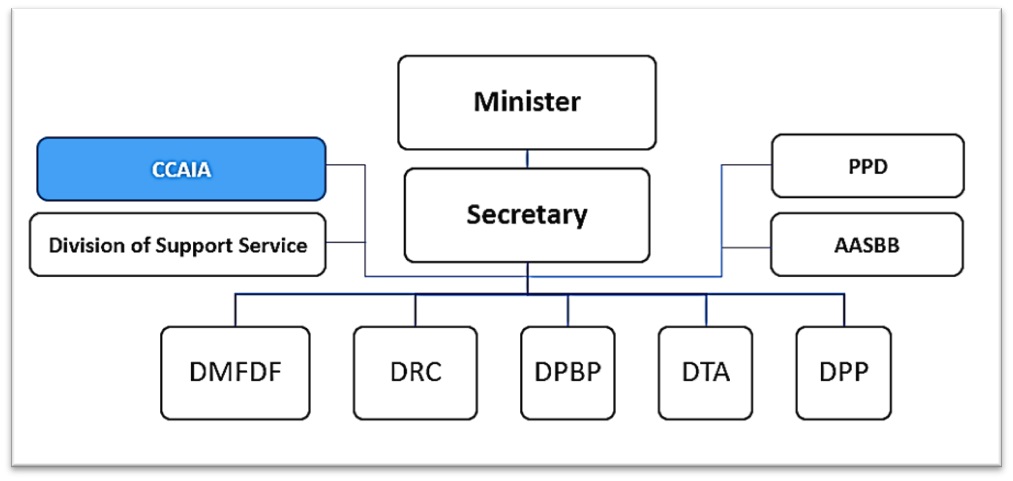

Organizational Chart for Ministry of Finance:

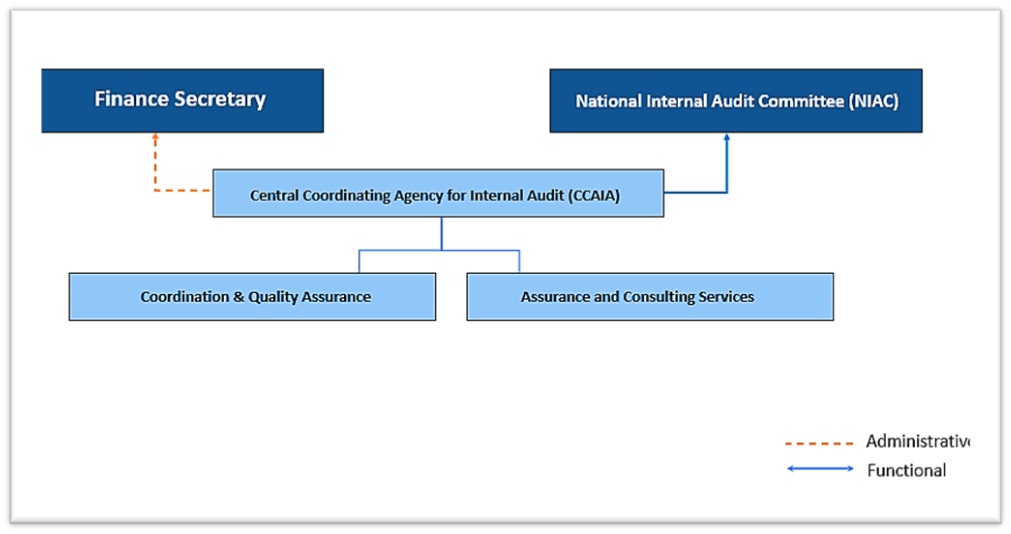

Reporting line:

The CCAIA reports administratively to the Finance Secretary and functionally to the chairperson of the National Internal Audit Committee.

In line with Section 23 (O) of the Public Finance Act of Bhutan 2007, the Central Coordinating Agency under the Ministry of Finance has the following core mandates:

A) Coordination and Quality Assurance:

- Coordinate the overall Internal Audit functions;

- Ensure quality assurance and improvement, uniformity and consistency of Internal Audit function;

- Prepare and issue periodic reports summarizing results of audit activities and the status of implementation of past audit recommendations to the National Internal Audit Committee and share a copy with the respective management for actions;

- Develop, review, and modify the Charter, Standards, Manuals, and Code of Ethics from time to time;

- Render technical backstopping and consultation to the Internal Auditors as and when required;

- Promote functional partnerships with the Royal Audit Authority, the Anti-Corruption Commission, and other relevant law enforcement agencies;

- Promote understanding, acceptance, and utilization of Internal Audit services by all levels of Management;

- Develop professional proficiency through enhancement of skills, techniques, and knowledge of Internal Auditors;

- Coordinate recruitments, transfers, promotions and develop career paths for Internal Auditors;

- Provide guidelines to Internal Auditors and ensure professional practice of Internal Audit;

- Protect Internal Auditors from undue reprisals for their professional conduct;

- Liaise with other national, regional, and international bodies for the development of Internal Audit Services in the country;

- Provide secretarial support to the National Internal Audit Committee which is the ultimate appellate body to the Internal Audit function in the country.

B) Assurance and Consulting Service:

- Develop an annual audit plan based on comprehensive risk assessment in consultation with the agencies and submit it to the National Internal Audit Committee for approval;

- Implement the approved annual audit plan following the Standards for Professional Practice of Internal Auditing, Charter, Internal Audit Manual, and the Internal Audit’s Code of Ethics;

- Provide consulting services for assignments/reviews requested by the agencies.

- Communicate the impact of resource limitations and significant interim changes in the plan;

- Issue reports annually summarizing results of audit activities and status of implementation of past audit recommendations to the management;

- Provide adequate follow-up to ensure corrective action is taken and report its status to the National Internal Audit Committee on half yearly basis;

- Consider the scope of work of the external auditors and other regulators as appropriate and collaborate with them to provide optimal coverage and avoid duplication of work.

13,833 total views, 1 views today